Let Me Clarify

Let Me Clarify

Sequence Risk and Buffer Assets

Sequence risk is something we’re all likely familiar with, even if we call it by another name. It’s based around the concept that money placed into and taken out of a fluid and changing market will vary in terms of growth and withdrawal percentage depending on the time in which the withdrawal occurs. For example, consider an investment which only allows investors to buy a share at a predetermined price (in this case, we’ll say $1) on a certain day. For this example, your share can only be redeemed with the issuer at maturity, at which point it’s worth a pre-determined value. This investment, essentially has no sequence risk. It doesn’t matter when you withdraw it, it’s always worth $1.

To contrast, let’s consider a portfolio held of moving assets, like stocks, that from the day you invest until the day you withdraw, that return is going to be largely determined by when those investments or withdrawals occur. There is a risk that you’re going to be buying at a high point and having to sell at a low point.

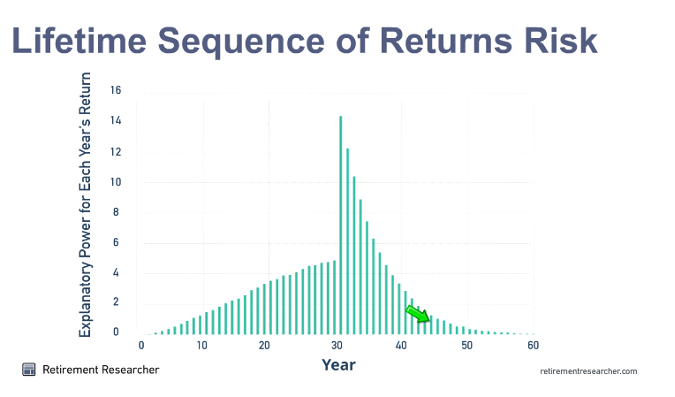

As an investor saving toward a retirement goal, it’s important to consider sequence risk when it comes to pre-retirement (putting money into savings) and post-retirement (taking money out). A study by Wade Pfau created the nice chart I’ve got below – I thought it was a nice visualization to this concept. It attempts to showcase the exponential impact of the portfolio’s return (i.e., stock market return) on the overall lifespan return of the portfolio. In this example, it’s showing an investor who begins investing for 30 years, retires, and dies 30 years later:

So what does this show us, exactly? To put it simply, each year we approach nearer to retirement, the influence that the market return of the portfolio will have on overall return of the portfolio from year 1 to year 60.

We see at the first year of retirement, year 30, that the market influence has a tremendous spike, indicating that this year in particular (and arguably those immediately following it), is going to dramatically affect the performance of this 60 year investment. This study is fairly easy to conceptualize- it’s the time where we stop putting money in and begin drawing money out. It’s the baseline where all the compounding of interest and return will begin for the next 30 years.

Imagine if you had decided to retire at the end of 2007- your first year of retirement, the market that would most strongly determine the financial health of your retirement, was 2008 when the S&P 500 returned -37%. Understandably, their retirement is going to have a much different look than they would have been projecting from just a year or two earlier.

Since we now understand how critical this is, how do advisors and investors combat against this type of risk? One strategy is to explore adding buffer assets into your portfolio- levers that can be pulled at certain times if certain situations present themselves. If you choose to consider a buffer asset to insulate against sequence risk, I would argue the best for this type of situation would be one where there are additional benefits. A common approach would be the purchase of an annuity, but that isn’t always the best solution. An annuity could potentially provide income to bridge a couple of bad market years, but I would argue that we have a lot of clients now who are holding annuities in their portfolio that are doing nothing except being subject to a lack of return in a booming market and incurring fees (I do think annuities have a value in a portfolio lacking guaranteed income, but that’s not the risk we’re considering here). Another option for a younger client would be a cash value life insurance policy, which early on would provide the benefit of life insurance, and at retirement have a cash value that could be accessible in the event of a poor market for withdrawal. Buffer assets allow us some flexibility with when and where to take our withdrawals and as we can tell from the chart above, this flexibility could potentially have a large impact on a retirement portfolio. As with everything when it comes to investing, it’s about tailoring a solution that fits into your specific situation.

As we embark on this clarifying journey together, we encourage you to submit any ideas, topics, or questions to info@clarifywealth.com. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and no guarantee of future results. All investing involves risk including loss of principal. No strategy assures success or protects against loss. All investing involves risk including loss of principal. No strategy assures success or protects against loss. There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk. Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss “Let Me Clarify” is our periodic blog containing Clarify’s insights and thoughts about a variety of topics. To learn more about Adam, click here