Let Me Clarify

Let Me Clarify

Homeowners Insurance and Inflation Walk into a Bar

Inflation is here, that’s no secret. News about rising prices on gas, food, cars, and most other goods we use is everywhere you turn. Literally everywhere. I can’t remember the last time I turned on the TV, scrolled through social media, or even got together with family or friends, where the topic of inflation wasn’t at least brought up in one way or another. Everyone has their own view on general inflation, so I don’t want to spend time on that. What I do want to spend time on is something most people don’t think about; the indirect effect that inflation has on homeowners’ insurance.

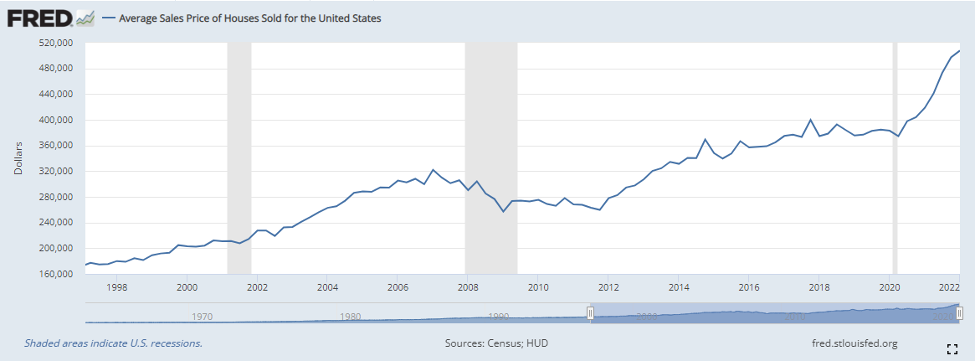

Even before general inflation was affecting most Americans, house prices were on the rise. According to research from the Federal Reserve Bank of St. Louis, average home sale prices have risen from $374,500 in Q2 of 2020 to $507,800 in Q1 of 2022. This is a substantial short-term increase compared to long-term averages. See below:

While current homeowners are certainly enjoying the increase in their net worth, everyone should also take this time to review your homeowner’s insurance.

Most insurance companies abide by the “80% Rule”. This means that for a home to be “fully insured”, it must have coverage equal to at least 80% of the home’s current value.

What does it mean to be “fully insured”?

When fully insured, insurance companies will cover approved claims up to your coverage amount. Let’s assume someone has $160,000 of coverage on a $200,000 home (80% covered). In this case, any claim up to $160,000 is typically fully covered. For example:

- If this homeowner has a claim for $120,000 in damages, insurance will likely cover the entire thing.

What if I’m not “fully insured”?

If not fully insured, most insurance companies will only cover an amount proportionate to the percentage you are covered. Let’s now assume that same $200,000 home is only insured up to $150,000 (75% covered). In this case, the insurance company will typically only cover 75% of any claim up to the maximum amount. For example:

- If this homeowner has a claim for $120,000 in damages, insurance will likely only cover $90,000 (75% of it), leaving him or her to cover the remaining $30,000 out-of-pocket.

This is where inflation comes in. Unless you’ve reviewed your homeowner’s coverage within the last year or two, recent increases in home values have likely pushed your coverage amount below 80% of what your home is currently worth.

Sticking with the examples above, the hypothetical homeowner with $160,000 of coverage is well underinsured today, if the home is now worth $260,000. With outdated coverage, it’s likely insurance will only cover 61% of any claims submitted. This could result in huge out-of-pocket costs relative to the increase in insurance premiums for adequate coverage.

There’s a slim chance that you initially had more than enough coverage to still be above the 80% threshold, but it is unlikely when home prices have increased ~36% (referring to the average house prices from the chart above), unless your policy was updated in the past year or so.

Insurance is something that nobody enjoys paying for…until they need it. So, I encourage you to at least review your coverage against the current value of your home to weigh the risks of being underinsured. Reviewing this every few years can also save you on paying unnecessarily high premiums on excess coverage, should prices stabilize and drop back to long-term average levels in the future.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendation for any individual.