Let Me Clarify

Let Me Clarify

CD Ladders

With interest rates on the rise this year, I’ve seen articles aimed at investors discussing more traditional fixed income style investments. These types of debt-focused investments like bonds and CDs had fallen out of fashion in the past several years because their coupon rates had dropped so low that they typically paid far less than incentivized cash accounts, like online savings. However, traditional strategies to employ them as an income generator in a portfolio have had a slight resurgence lately, and it’s a topic I’ve always been fascinated by.

This article will focus on a common strategy used with Certificates of Deposit, or CDs. To make sure we’re all on the same page, here’s a brief refresher on how and why CDs work. Simplified, you’re lending your cash to a borrower (typically a bank) who promises to pay you back after a certain interval. While they have your money, they’re paying you interest, which is locked in for the duration of the loan at the time of purchase. CDs, when held at a bank, are insured against loss by FDIC insurance up to $250,000 (per account, per owner) and pay a fixed income amount, called a coupon rate, a certain number of times per year. One of the apparent disadvantages to using a CD is that your money is essentially locked up for the term of the CD. If, for instance, you purchase a CD for 5 years that pays you 3% per year, and in 6 months a new 5-year CD is available that pays 6% per year, you’re not going to feel good about having your money locked into the first one. So, a widely used strategy, called laddering, can help to offset these types of illiquidity and rate risks.

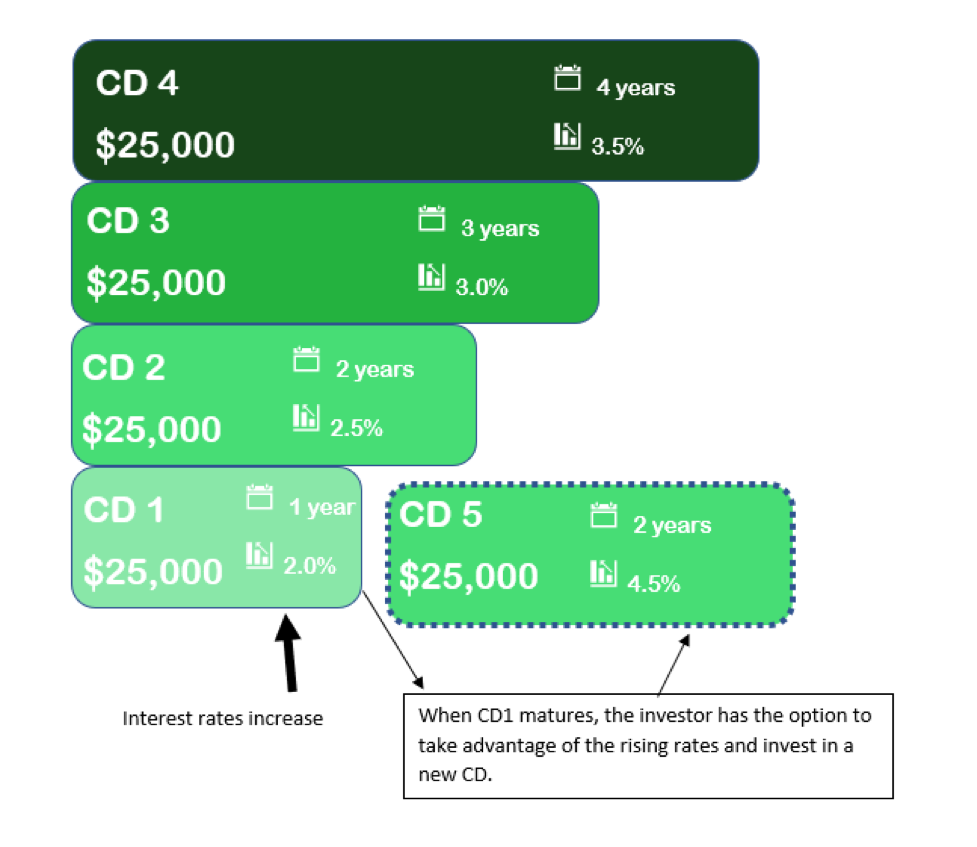

Laddering is a simple concept, and depending on your brokerage firm or bank, can be an easy strategy to implement. Often the most difficult part is just knowing it exists and asking for help to implement it. Building a CD ladder involves staggering term maturities, and allowing those to be reinvested along the way for the duration of the ladder. Let’s illustrate with the following scenario:

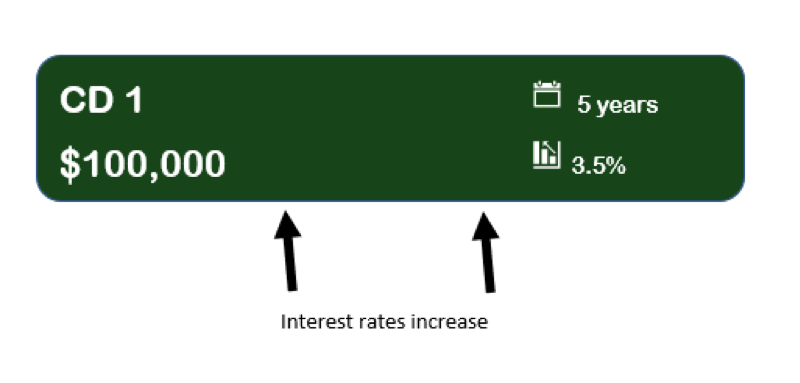

An investor needs to have $100,000 of their savings available for a major purchase in 5 years but wants to earn money on that principal until that point. They could purchase a 5-year CD and lock their savings into a fixed coupon rate for the next 5 years. If this investor had an emergency come up and needed some of these funds, they would likely have a large surrender fee to pay for withdrawing their money early, often large enough to wipe out any interest they would have earned to that point.

Additionally, if interest and coupon rates rise on new CDs, they are unable to take advantage, since their rate is locked in for the length of the CD term.

An alternative, which can help to reduce some of these risks, would be laddering their investment. This strategy ensures that if rates have risen between the initial investment and the first maturity, they can take advantage of the now higher rates by purchasing a new CD, and can continue to do so as each CD matures until they need the funds for their purchase.

Often a CD ladder is a strong strategy in a rising interest rate environment. In the above graphic, if the investor had not chosen to ladder their CDs, they would be unable to take advantage of the interest rate increase indicated by the heavy black arrow. By laddering, at the first CD maturity date, the investor is given additional flexibility with a portion of their funds, while still seeking return.

As with the purchase of any investment product, we encourage you to talk with a qualified financial professional to answer any questions that you may have.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendation for any individual.