Insights

Tax Considerations for Stock Options

(This is part two of our series on Stock options; if you haven’t read part 1, click here first!)

NQSOs vs ISOs

When a company decides to grant stock options, rather than outright stock to an employee, they have a couple of choices of what type of options to grant. Depending on whether the stock options are non-qualified (NQSOs) or incentive stock options (ISOs) will result in a difference in terms of taxes paid by the company, as well as taxes paid by the recipient.

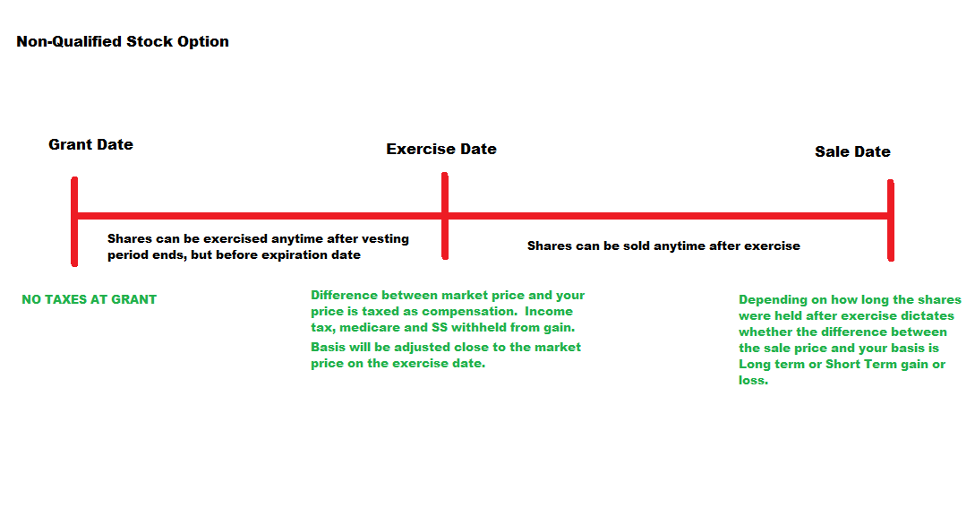

Taxation of NQSOs

Non-Qualified Stock Options (NQSOs) are by far the most common type of stock option award. Their taxation is straightforward and doesn’t qualify for any special tax treatment. When the options are granted, there is no taxable event to the recipient. Tax is assessed at the time of exercise. The difference between the value of the shares after exercise and the price paid on the exercise price is called the bargain element, and it’s simply treated as compensation. For example, if you are granted 100 shares at an exercise price of $50 (value of $5,000), and you exercise when the price of the stock is $100 (value of $10,000), the bargain element is $5,000. Interestingly, in most cases at the time of exercise, income taxes, Medicare taxes, and Social Security taxes are all withheld, just as if it were income from your paycheck. If they aren’t taken out at the time of exercise, they will be due when you file your tax return as the bargain element is reported on your W2.

At this point, the recipient no longer holds options, but rather shares of the stock, which has triggered reportable (taxable) income. However, since you paid income tax on the bargain element, the basis is adjusted to the cost of the stock (exercise price) PLUS the compensation you’ve already been taxed on. This results in a cost basis close to what you’d have paid if you bought the shares outright in the market.

A second tax event occurs at the time of sale. Since you purchased the shares on the date of exercise, any gain or loss on shares sold within one year are considered short term. Any shares sold after the one year mark qualify for long term gain or loss treatment. Since your basis in the stock at the time of exercise should be very close to the price you sell at, typically a cashless exercise (again where you exercise and sell a portion of the shares immediately) has very minimal short term gain or loss implications.

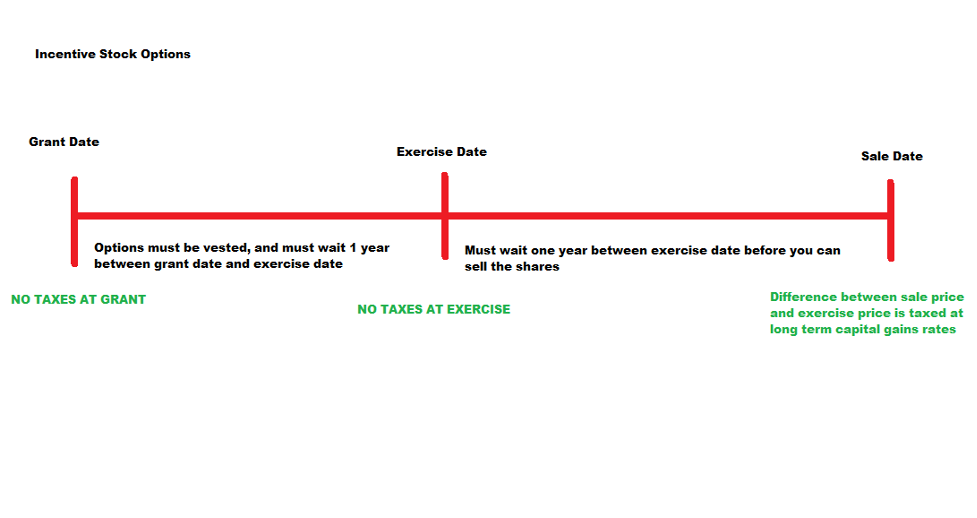

Taxation of ISOs

Much like NQSOs, there is no taxable event triggered at the time of grant. However, there is also no tax event that triggers at the time of exercise either* (It should be noted that this exercise can be taxable on an ISO if you are subject to the Alternative Minimum Tax. It’s a complicated scenario, and I’m not going to get into it here as I don’t think the likelihood of needing to know it is very high, but if this applies to you, just give us a call).

The tax implication begins when you sell the shares. ISOs get favorable tax treatment, and as such, have rigid rules that must be followed or they lose their special tax standing. The first is that ISOs, regardless of vesting, cannot be exercised within one year of the grant date. After exercising, if you choose to sell within one year of the exercise date, the bargain element is taxed as ordinary income. Holding it beyond the one year mark qualifies the entire gain above the exercise price as a long term capital gain, rather than ordinary income. So while the NQSOs are going to be assessed as compensation and have withholdings/taxes due at the time of exercise, by waiting to exercise an ISO for one year after the grant date, and then waiting to sell the shares for an additional year after the exercise date, you benefit from a lower tax rate on the difference.

Wrapping up

In most cases, if you’re considering action on an employer stock plan, it’s a wise suggestion to enlist help from a CFP or CPA before exercising or selling any investments. The strategies and rules regarding these plans can be complex and difficult to navigate, and taking action without understanding the impact can result in some big surprises at tax time, which no one likes. If you read this and want more information about your specific situation, give us a call or an email, we’re happy to help.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendation for any individual. All investing involves risk including loss of principal. No strategy assures success or protects against loss.